If you're looking to expand your workforce or are struggling to retain or improve your current workforce, these job tax credits could strategically assist and help grow your business.

This federal tax credit provides tax savings to companies who employ individuals that face significant barriers to employment with savings up to $2,400/employee.. You may qualify for this credit if you have first and/or second year wages paid to or incurred for targeted groups during the tax year.

WOTC-Eligible Worker Categories:

Type: Nonrefundable

Dates: Jan 1, 2015 - Dec 31, 2025

Claim Process: Request certification by filing IRS Form 8850 with the state workforce agency within 28 days after eligible workers begin work. Calculate the credit using Form 5884, Work Opportunity Credit, and include it when filing your federal income tax return.

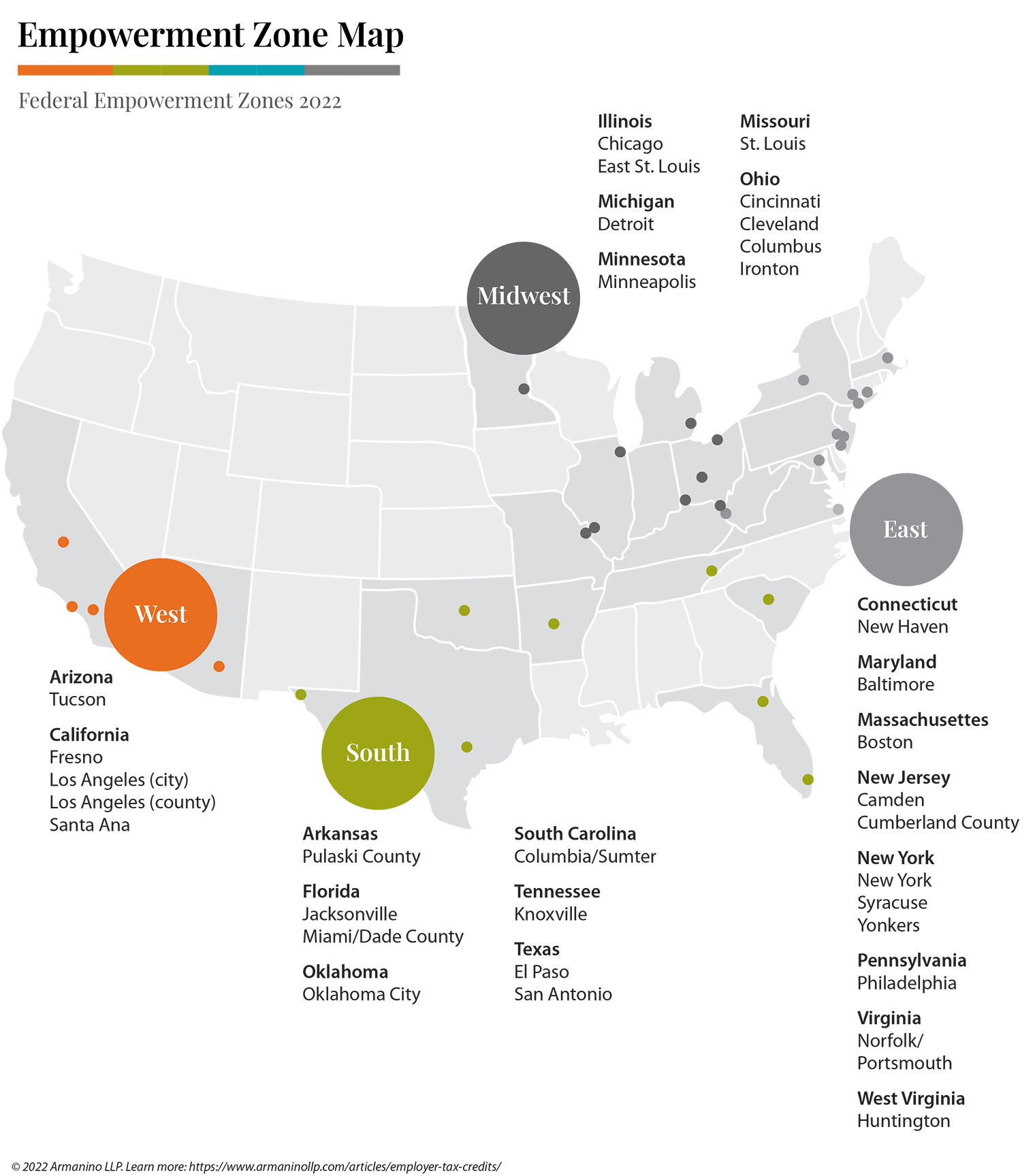

This federal tax credit incentivizes hiring individuals that live and work in designated Empowerment Zones (EZs) -- economically distressed areas identified by the federal government to encourage economic development in low-income and high-poverty areas. Empowerment Zones are one of three U.S. congressional designations that make up the Empowerment Zone Program to aid distressed urban and rural communities – the other two being Enterprise Communities (ECs) and Renewal Communities (RCs).

Employers eligible for Empowerment Zone tax credits can receive .20% of their qualified zone wages paid or incurred (up to $15,000 savings) during the calendar year for services performed by an employee while the employee is a qualified zone employee. See IRS Form 8844 for qualifying empowerment zone employees and wages.

Type: Nonrefundable

Dates: 1993 - Dec 31, 2025

Claim: File Form 8844, Empowerment Zone Credit with quarterly federal employment tax returns.

Use the map below to find empowerment zones located near you.

This federal tax credit is available to employers who hire Native Americans or spouses of Native Americans living on a reservation or working for an employer on that reservation. It entitles the employer to a 20% tax credit on qualified income and benefits.

Type: Refundable

Dates: Effective through Dec 31, 2021

Claim Process: File Form 8845, Indian Employment Credit federal tax credit if you paid or incurred qualified wages and/or qualified employee health insurance costs to or for a qualified employee during the tax year. Note that partnerships, S corporations, cooperative, estates and trusts must file this form. All others can claim this credit directly on Form 3800, General Business Credit.

This federal tax credit worth up to $10,000 per employee, is intended to keep employees affected by the ongoing COVID-19 pandemic on the payroll even if they are not working during the covered period. To qualify, employers must prove that they either partially or fully suspended operations due to a COVID-19 shutdown, or that they experienced a significant decline in gross receipts. See Employee Retention Credit for more details.

Type: Partially-Refundable

Dates: Mar 13, 2020 - Jun 30, 2021

Claim Process: Report total qualified wages and the related health insurance costs on quarterly federal employment tax returns, Form 941.

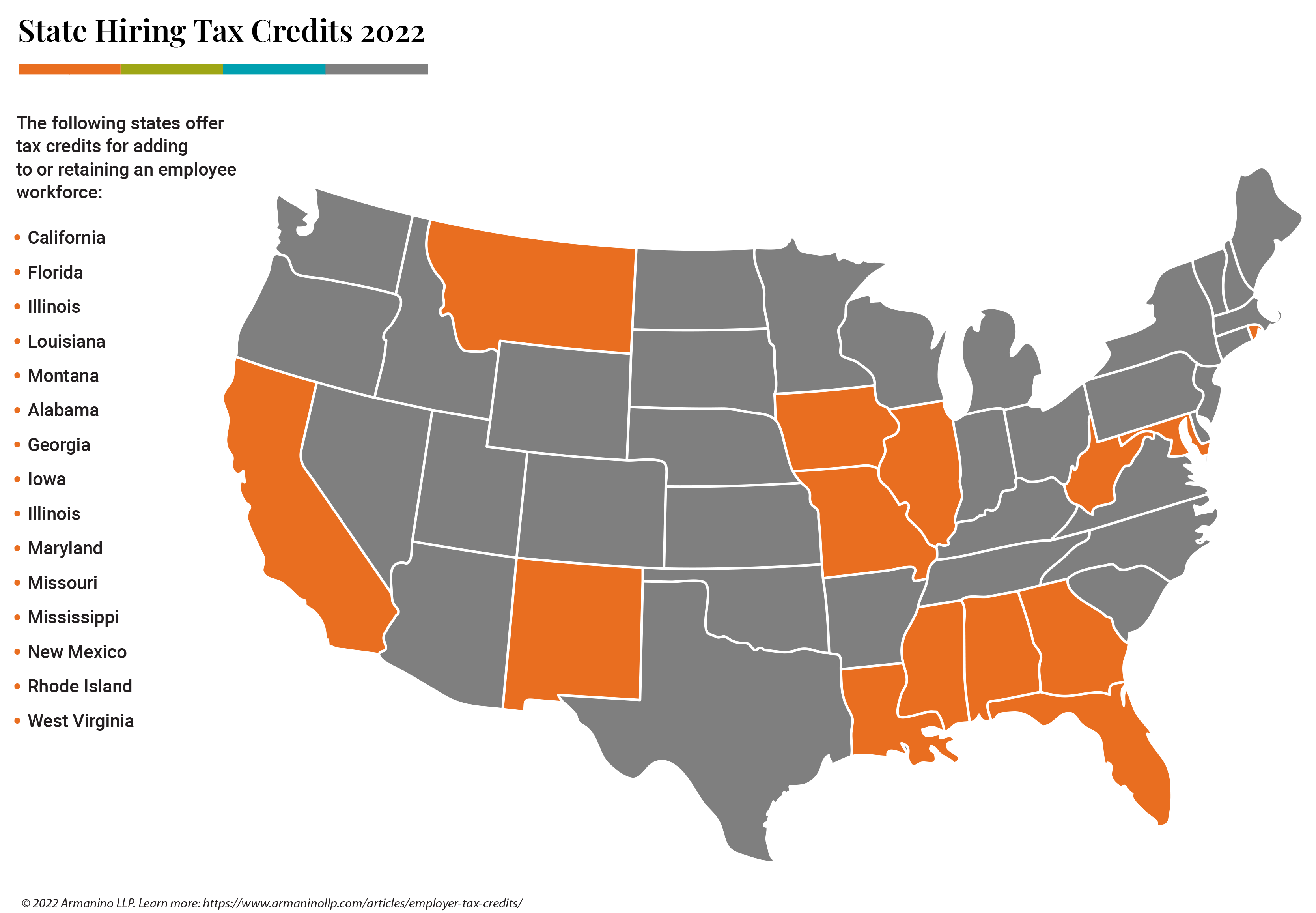

In addition to federal tax credits, some U.S. states additionally offer tax credits for job creation and employee retention.

States that currently offer hiring tax credits include:

It is possible to combine state and federal tax credits. Employers may be able to save the full amount for both state and federal tax credits. However, it depends on how the credit is calculated. Wages, for example, can’t be double dipped. It also depends on the state credit itself and whether it is calculated on a standalone basis or based on the federal credit.

Generally, combining credits is done at each level, combining at the federal level and combining at the state level. You can have both a federal credit and a state credit – R&D tax credits are a great example of this. WOTC is a federal credit and doesn’t have a separate state credit; however, some states will allow a deduction of the federal piece of the credit that was disallowed.

Do you provide training programs or professional development for your employees? Check out these tax credits available to improve the return on your people investment.

This federal tax credit saves 25% of qualified expenditures paid for employee-provided childcare -- up to $150,000 maximum credit savings per year. Employers themselves may also be eligible to receive the same benefits as their employees if the company is incorporated.

Type: Refundable

Dates: No expiration currently defined.

Claim Process: File Form 8882, Credit for Employer-Provided Childcare Facilities and Services with annual federal income tax returns.

This federal tax credit (also known as "Credit for Small Employer Health Insurance Premiums") applies to employers paying at least half of the premiums for their employees’ health coverage. It saves up to 50% of employee health coverage expenses for qualifying employers that meet certain criteria and purchase coverage through the Small Business Health Options (SHOP program. This credit only applies to companies who employ fewer than 25 employees and pay average wages of less than $50,000 a year.

Type: Refundable

Dates: No expiration currently defined

Claim Process: File Form 8941, Credit for Small Employer Health Insurance Premiums with annual federal income tax returns.

This federal tax credit could save you up to $500, or 50% of your startup cost, if you plan on building a pension plan for your employees. To qualify, your company must employ 100 or fewer people who have received at least $5,000 in compensation, and you haven’t had an existing 401(k) or other retirement plan in place for at least three years. You can claim this credit for the first three years of your pension plan.

Type: Nonrefundable

Dates: No expiration currently defined.

Claim Process: File Form 8881, Credit for Small Employer Pension Plan Startup Costs with your annual tax return.

This federal tax credit applies to the cost of mine rescue training programs -- either paid or incurred -- saving up to $50,000 for each qualified employee. Employers may claim this credit if they employ individuals as miners in U.S. underground mines.

Type: Nonrefundable

Dates: Effective through Dec 31, 2022.

Claim Process: File Form 8923, Mine Rescue Team Training Credit with annual federal income tax returns.

There are several different credits available for employers offering paid leave to their employees, ranging from incentives for sick leave to vaccination leave to family leave to everything in between. Take a look at the credits outlined below.

This federal tax credit, meant to alleviate the burden of military deployment, is available to employers offering differential pay to employees entering activity duty uniformed service in the U.S. This credit saves 20% of up to $20,000 of differential pay made to eligible employees. (i.e. Up to $4,000/active duty employee).

Type: Nonrefundable (part of the general business credit)

Dates: "Effective after 2008.

Claim Process: File Form 8932, Credit for Employer Differential Wage Payments with annual federal income tax returns in 2021 or later. For earlier tax years, use the applicable prior revision of this form.

This federal tax credit also known as the Credit for Portion of Employer Social Security Paid with Respect to Employee Cash Tips, typically equals the amount of employer social security or Medicare taxes paid on or incurred by the employer on tips received by the employee (i.e. Save up to 7.65% of reported tips). It is only available for employers working in entities where tipping is customary for providing food or beverages.

Type: Nonrefundable

Dates: No expiration currently defined.

Claim Process: File Form 8846, Credit for Employer Social Security and Medicare Taxes Paid on Certain Employee Tips with annual federal income tax returns.

This federal tax credit, which applies to qualified employers who paid leave to an employee for family or medical-related reasons, could save between 12.5% and 25% of the leave pay you provided, depending on the employee’s pre-leave pay. To qualify, the employee must have been on your payroll for at least one year and you must have provided leave pay for at least two weeks. See the IRS FAQ for more information.

Type: Refundable

Dates: Dec 31, 2017 - Dec 31, 2025

Claim Process: File Form 8994, Employer Credit for Paid Family and Medical Leave with annual federal income tax returns.

This federal tax credit reimburses employers with fewer than 500 employees for the cost of providing paid sick and family leave because of the COVID-19 pandemic. The sick leave credit is worth up to $511 per day per employee for up to two weeks, and the family leave credit is worth up to $200 per day for up to twelve weeks. Maximum credit savings of $5,110/employee. See IRS Covid-19 Employee Paid Leave for more details.

Type: Refundable

Dates: Apr 1, 2021 - Sep 30, 2021

Claim Process: Report paid sick and family leave wages on Form 941, Employer's Quarterly Federal Tax Return.

This federal tax credit allows qualified employers with fewer than 500 employees to be reimbursed for the cost of providing paid leave to receive or recover from COVID-19 vaccines. Employers can receive up to $511 per day for each vaccinated employee. See IRS Covid-19 Employee Paid Leave for more details.

Type: Refundable

Dates: Apr 1, 2021 - Sep 30, 2021

Claim Process: Report paid vaccination leave wages on Form 941, Employer's Quarterly Federal Tax Return.

Mistakes can result in amended returns, added expenses, or missed credit opportunities. Avoid these common filing mistakes when claiming hiring tax credits:

1) Using the wrong tax form

Business tax forms vary based on your legal structure. Read the IRS website carefully to ensure that you are using the correct form for the credits you’re looking to claim.

2) Missing credits that you are eligible for

Your goal as a business should be to make sure you are exploring all possible avenues for potential tax savings. Using a reputable accountant or other knowledgeable tax professional is a great way to make sure nothing is overlooked during the filing process.

3) Not informing third-party vendors

To avoid processing delays or balance due notices, employers using third-party vendors must ensure that they informed those vendors of any tax credits paid or requested.

4) Reporting advances requested instead of advance payments of credits received

If an employer has requested an advance payment of a tax credit but hasn’t yet received it, it should not be reported on their tax Form 941. Conversely, if an employer receives an advance payment but doesn’t report it on Form 941, they may receive a balance due notice.

Hiring tax credits can have a substantial impact on your business’s federal tax liability. By taking advantage of the tax credits outlined above, you can simultaneously meet your business needs, offset business expenses and invest in your people.

Employers need to have a process in place to determine whether potential employees would qualify for tax credits. This process is time sensitive. For WOTC, for example, you have only 28 days to notify state agency of hire. If you miss that deadline, you lose the credit.

To ensure you’re not missing out on potential tax credits, include a behind-the-scenes screening process for WOTC with your regular hiring process. You can also send in appropriate pre-certifications to ensure you remain ahead of the game, covering all your bases for any potential credits that could be out there.

For assistance with claiming employer tax credits, understanding credit calculations or determining whether you qualify, check out our tax credit services.

Armanino has the industry expertise, tax credit experience and track record of customer satisfaction to best advise your tax credit incentive strategy and compliance needs.

Contact us today for a free assessment.