Just like the tax law revamp and the new revenue recognition standard, there’s another major new accounting standard that will potentially disrupt the status quo for accounting departments in public, private and nonprofit entities.

ASC 842 is the new lease accounting standard, and it represents the most significant change to lease accounting in 30 years. Impacting nearly every company that leases something — including real estate, vehicles, equipment, furniture and more — the standard aims to bring operating leases onto the balance sheet for the first time.

Among the implementation challenges, for organizations of all sizes, is the time-consuming effort of collecting and analyzing lease data from contracts across the business. Major changes to lease management processes may be required as well, and new technology could be necessary to handle data management, calculations and compliance reporting.

While the effective date for calendar-year-end public companies is January 1, 2019, calendar- year-end private companies have until January 1, 2020. Judging by the numerous reports of public companies that have struggled to comply, private companies should waste no time in getting started.

This white paper can help. In it, you’ll learn the basics of ASC 842 (including core intents and principles) and the challenges you might face in preparing for adoption. We’ve also included an adoption checklist to help you get going.

The overarching intent of the new lease accounting guidance from the Financial Accounting Standards Board (FASB) is to achieve greater transparency and address off-balance-sheet financing concerns related to lessees’ operating leases.

According to the FASB, the ASC 842 guidance improves lease accounting by:

Under ASC 842, companies will now be required to recognize the majority of leases as assets and liabilities on their balance sheet for all financial reporting. The new standard also expands qualitative and quantitative disclosures, including: the nature of leases, significant judgments and assumptions, lease expense amounts and maturity tables.

There are no scope exceptions for smaller leases (i.e., leases of low-value assets such as personal computers or copiers). The new standard applies to all identifiable assets, except:

| FOR LESSEES | FOR LESSORS |

|---|---|

| Operating leases (for right-of-use assets now appear on the balance sheet | Fewer leases will be classified as direct financing |

| Lessees will recognize both operating and finance leases on the balance sheet | Fewer upfront costs (initial direct costs) will qualify for deferral |

| Organizations will recognize a right-of-use asset and lease liability | Unusual outcomes may result when sales-type leases contain primarily variable consideration |

| New financial statement disclosures are required | New financial statement disclosures are required |

The new lease accounting guidance aligns the underlying principles of the new lessor model with those in ASC 606, the new revenue recognition standard. For example, ASC 842 requires lessors to use the guidance in ASC 606-10-32-28 through 32-41 when separating and allocating consideration to the components in a contract. For this reason, some organizations are choosing to adopt both new standards at the same time, rather than implement them sequentially.

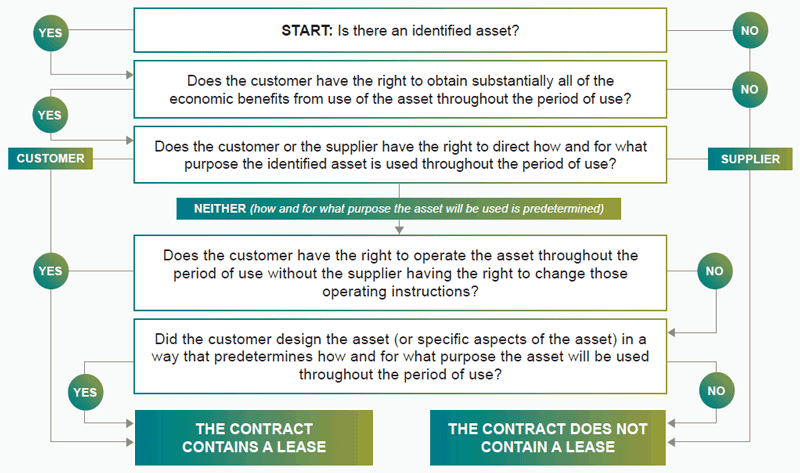

A contract is (or contains) a lease when two criteria are met:

Along with having more time to comply, private companies also have the advantage of learning from the efforts and mistakes of public companies that have had to move sooner to implement the standard.

Numerous surveys have noted that many public companies underestimated the effort and manpower required to implement the new lease accounting rules.

Whether your company has dozens, hundreds or thousands of leases, your team could face some of the same challenges that affected public companies, including:

ASC 842 Lease Decision Flowchart

For many companies, the implementation of ASC 842 will not be a trivial matter given the extent of the changes, particularly for lessees. It’s imperative to begin implementation planning as early as possible to allow for unforeseen delays and stumbling blocks.

Developed for CFOs and their teams, the following checklist includes actionable steps to help as you begin planning and assessing your organization’s compliance efforts. If you have already begun implementing the new standard, the checklist may provide new ideas or approaches to help you avoid common pitfalls and stay on track for meeting the compliance deadline.

|

1. ASSESS REQUIRED RESOURCES While some organizations may have enough staff hours and in-house leasing knowledge to undertake the entire compliance initiative, many will not. |

Based on a preliminary understanding of the number of existing leases to be collected and analyzed from across the company, CFOs should determine whether external resources need to be obtained to handle all or part of the initiative, particularly the more resource-intensive activities such as lease abstraction and implementing new technology. |

|

2. IDENTIFY EXISTING LEASES With your project team in place, you’ll need to begin by locating all of your company’s lease documents. |

This typically involves working across departments and business units to survey all relevant areas about the existence of leases. As you collect the lease documents, initial analysis of the leases should help you uncover the accounting, operational or data issues you’ll need to resolve. |

|

3. EXAMINE FOR EMBEDDED LEASES |

Your team also needs to review service contracts, analyze them for embedded or implied leases and document them for your auditors. |

|

4. UPDATE LEASE INVENTORY |

Once you’ve collected all of the leases, including embedded leases, create or update a complete lease inventory. This will serve as your starting point for collecting all of the relevant data you’ll need for ASC 842 compliance. |

|

5. IDENTIFY DATA GAPS Reconcile the lease data you have in current systems or spreadsheets with the data points that you’ll need for compliance. |

For many companies, lease data such as the market value of a leased asset or discount rate was not previously tracked or needed for financial reporting, creating a gap in data for existing leases. Your goal is to identify all of the missing data types and create a plan for how to obtain the data for current and future leases. |

|

6. VALUATE THE IMPACT With lease inventory and information collected, you can begin assessing the impact of the new standards on your company’s financial statements, ratios, metrics and debt covenants. |

Work with stakeholders, such as investors, banks and external auditors, to disclose the expected impact and mitigate any risk associated with it. For instance, if debt covenants are likely to be affected, work with lenders to avoid violations. |

|

7. ASSESS AND REVISE INTERNAL CONTROLS AND POLICIES Your company may need to make significant process changes to comply with ASC 842. |

You’ll need to evaluate and redesign processes across departments. For example: managing changes to terms in existing lease contracts, or changing the workflow for new contracts so that accounting can identify and track leases and lease data. This step is an important part of planning for your future state of compliance after the FASB deadline. |

|

8. IDENTIFY AND DEPLOY SUPPORTING TECHNOLOGY |

Relying on manual efforts to collect, manage and track lease data, perform calculations, and create reports for compliance can be labor intensive and error prone for any company with more than a handful of leases. For that reason, many organizations are deploying new technology such as lease accounting or lease management software to automate as much of the lease accounting effort as possible. |

|

9. ABSTRACT AND STORE LEASE DATA This step will likely take place in parallel with some of the other steps, as it’s easily one of the most labor-intensive and time-consuming activities. |

You’ll need to analyze every existing lease contract and extract and store all the relevant data points. For lengthy contracts, such as real estate lease documents, a detailed examination of the document could take two to three hours of effort. Allot time for collecting additional necessary data that is not found in the individual contract, such as the discount rate. |

|

10. REVIEW AND REVISE FOR ONGOING COMPLIANCE Once the implementation project is complete, you’ll need to maintain compliance going forward. |

Take time to review the effectiveness of your policies and processes around lease management, the accuracy and completeness of the data you’re collecting, the effectiveness of the software you’ve deployed, and the impact of the new lease accounting requirements on your staffing levels. |

The New Lease Accounting Process

For each lease your organization identifies, you should:

While the new lease accounting standard will probably require significant time and effort to implement for all but the smallest companies, there are benefits in addition to compliance. You may identify unused leases, helping you free up cash. Analysis of lease data could provide the insight you need to improve lease negotiations and outcomes in the future. You could also gain deeper insight into leasing costs to help you make better decisions.

Private companies are in the enviable position of not only having more time to comply with ASC 842 than public companies, but also being able to learn from the mistakes of their public counterparts and apply what have proven to be best practices for expedient, effective compliance. But these advantages only exist for organizations that heed the warnings of the companies that have already achieved compliance. Don’t underestimate the effort and time required to adapt to this complex set of accounting and lease management changes.

The clock is ticking for private companies. There’s no time to waste in getting started with ASC 842 so you can enjoy the benefits of compliance while mitigating the impact and risk to your business.